Despite initial criticism, NAV loans are gradually being seen as an important financing tool for sponsors, says Doug Cruikshank, managing partner and founder of Hark Capital.

Increasing market recognition and acceptance of NAV loans

When we started Hark in 2013, almost no one had heard of NAV loans; the term itself hadn’t even been coined yet. Fast forward 11 years, NAV loans have become a recognized asset class. Large, blue-chip private equity funds, as well as middle market private equity funds, now have approximately $150 billion in NAV facilities outstanding, according to S&P Global. Not to mention growth equity, VC and secondary funds.

Major news outlets like the Wall Street Journal, Bloomberg and the New York Times have covered this no-longer-new tool, albeit not always in a positive light. While drama sells more papers, most NAV loans are straightforward: capital to improve the performance of portfolio companies. Like other new financial instruments, NAV loans are sometimes viewed with apprehension at first, followed by a more nuanced understanding of their appropriate uses.

Market demand for NAV loans has been highly correlated with PE M&A activity and cheap leverage availability, both of which drive sponsor exits. According to a June 2024 report by Ganymede Capital, exits decreased from $1 trillion in 2021 to $438 billion in 2023. The other key driver of exits is purchase multiples, which were high prior to the run-up in interest rates.

High Rates Driving NAV Loan Growth

The recent high interest rate environment and lack of exits have resulted in a compelling need to support buy-and-build platform growth and for non-dilutive support capital for overlevered portfolio companies. As they say, necessity is the mother of invention, and the need to help existing portfolios resulted in the rise of the NAV loan market.

What was previously an unknown tool became an instrument of choice for many sponsors. However, the increase in adoption did not occur right away, as the M&A and financing markets continued chugging away during 2020 and 2021 throughout the pandemic and the market was not yet accustomed to the NAV loan product.

As market adoption grew during 2022 and 2023, critics of NAV loans began to worry about potential misalignments between LPs and GPs with respect to this new tool. When using NAV loans for an LP distribution, some market participants claimed that NAV loans artificially inflated DPI figures which GPs hoped would aid in current fundraising efforts, but which added more leverage into the system.

Certain LPs felt that this use of proceeds allowed GPs to send LPs their own money back without having generated a true portfolio company exit, while at the same time lowering overall fund MOICs after considering the added interest cost. Other critics claimed that growing or protecting a portfolio company should only be done on a stand-alone basis, rather than tapping the value of the rest of the portfolio, a viewpoint that others countered was unfairly ignoring the NAV loan’s superior cost of capital.

Our view at Hark Capital is that like any tool, NAV loans can be used for “good or evil.” Our mission is to improve the returns of a sponsor’s portfolio, to the benefit of the sponsor’s LPs, not to enable the gaming of DPI or carry. Historically, approximately half of our transactions have been defensive, safeguarding portfolio company value, with the rest to support growth opportunities, often facilitating accretive add-ons. In short: we view NAV loans as increased optionality for sponsors.

Fighting Skepticism

Perhaps the most strenuous objection to NAV loans came from LPs who were surprised by them afterwards and didn’t even realize their (sometimes dated) LPAs allowed them. Surprise created skepticism and thus transparency became the watchword. We believe in full upfront disclosure of the NAV loan to the sponsor’s LPs. In our experience, when a GP brings a NAV loan request to its LPAC, if the rationale is sound, the LPs are overwhelmingly supportive. When it is not, the transaction (rightly) dies. The best practice to avoid LP misalignment concerns is clear communication. Quoting a recent Rede Partners report, 59 percent of LPs do not think they receive enough disclosure with regards to NAV facilities. Former Supreme Court Justice Louis Brandeis once said, “sunlight is the best disinfectant.” We agree.

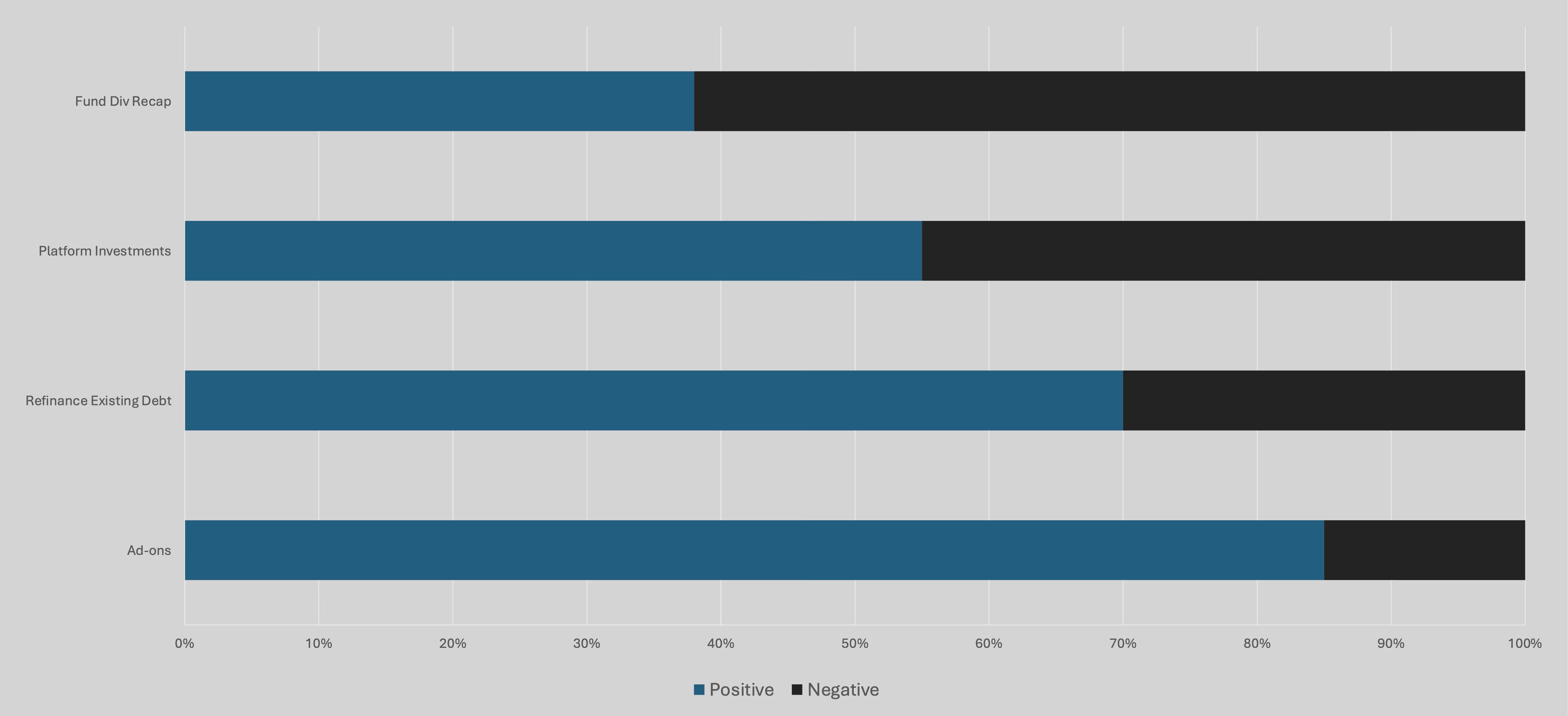

These views are echoed in recent LP surveys. According to the same Rede Partners report, LPs are supportive of “money in” transactions: add-ons (86 percent support), refinancing debt of a portfolio company, particularly if the cost of capital is lower than dilutive capital (71 percent support) and to a lesser degree, new platform investments (53 percent support). On the other hand, only 38 percent of surveyed participants are supportive of using a NAV loan for a fund dividend recap.

Like other new tools in the market, NAV loans are following the well-trodden path of skepticism then acceptance. Obstacles to adoption include lack of familiarity with the new technology and not understanding the appropriate (and most common) uses. Other tools that were initially unpopular with investors and later gained broader acceptance include subscription lines, secondary private equity sales and continuation vehicles (formerly referred to as “fund restructurings,” reflecting the initial skepticism of that product).

NAV loans, used appropriately and with proper disclosure, provide creative, cost-effective solutions to sponsor portfolios. The recent run-up in purchase multiples combined with the far less benign interest rate environment have underscored the importance of the NAV loan product. As GPs and LPs continue to codify their communication protocols, NAV loans will become less controversial and will take their place alongside subscription lines and continuation vehicles as an important financing tool for sponsors.