The second quarter of 2025 began with continued uncertainty surrounding tariff policy, but the increasing crystallization of policy and investor confidence in the US economy’s resilience, as seen in public markets reaching all-time highs, led to a rebound in deal activity and company performance towards the end of the quarter. With deal activity potentially picking up and buyout multiples still below 2021 and 2022 highs, NAV lending provides a non-dilutive source of capital for sponsors with limited dry power looking to make acquisitions.

Drivers of Demand

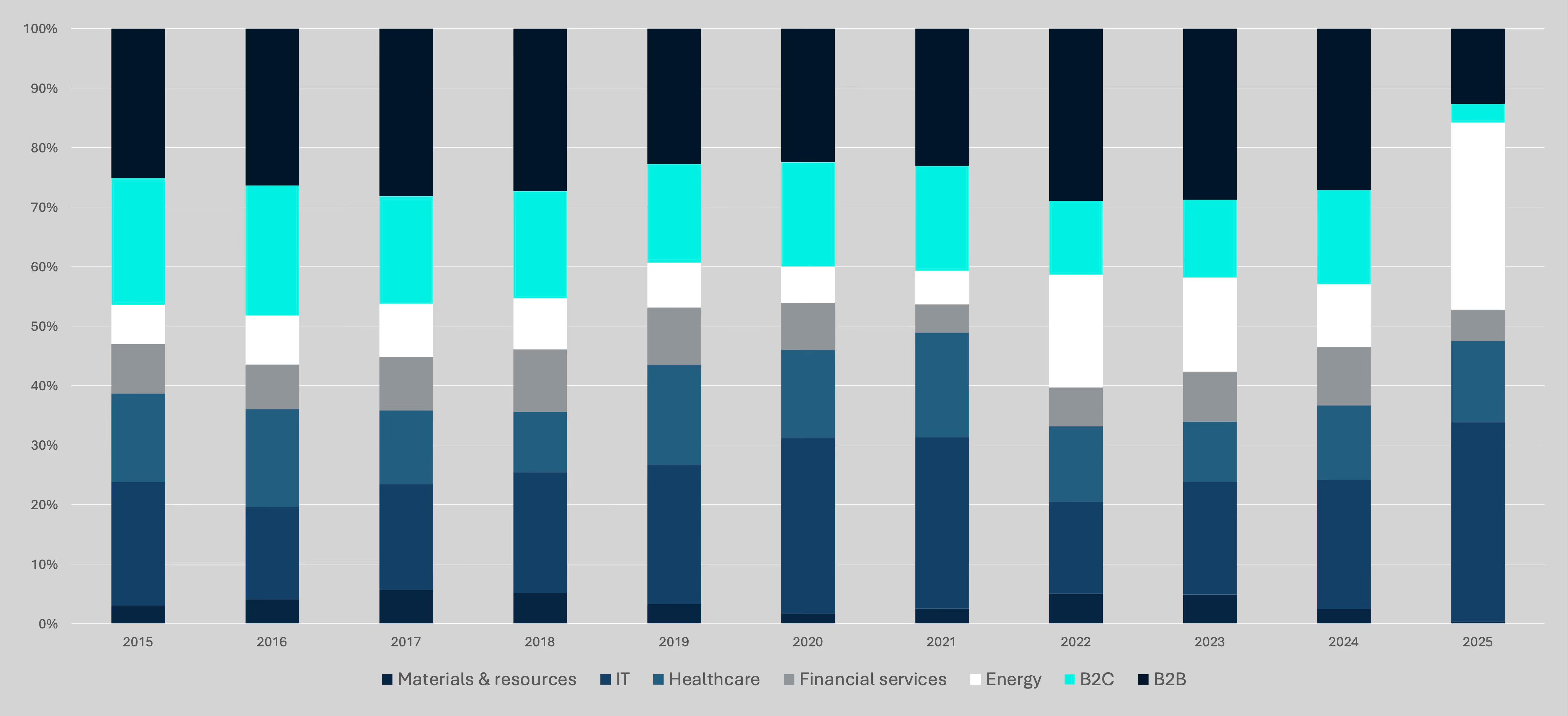

Tariff uncertainty in H1 2025 disproportionately impacted certain industries with B2B and B2C companies faring worse than others given their direct exposure to imports.

The chart below shows that B2B and B2C companies represented only ~16% of exit value in 2025 through Q2. This combined total represents a steep decline from 2024 when the industries combined for ~43% of exit value, and the lowest combined total since Pitchbook began collecting the data in 2011. The limited exit activity in the B2B and B2C industries reflects the significant recent headwinds faced by these industries and corresponding impact on their valuations and investor appetite.

What this means for NAV lending: A challenging exit and operating environment, particularly for certain industries, will require sponsors to inject capital into underperforming portfolio companies. Demand for NAV facilities will increase as mid-to-late stage funds with limited dry powder seek to protect and grow portfolio NAV in a difficult exit and fundraising environment.

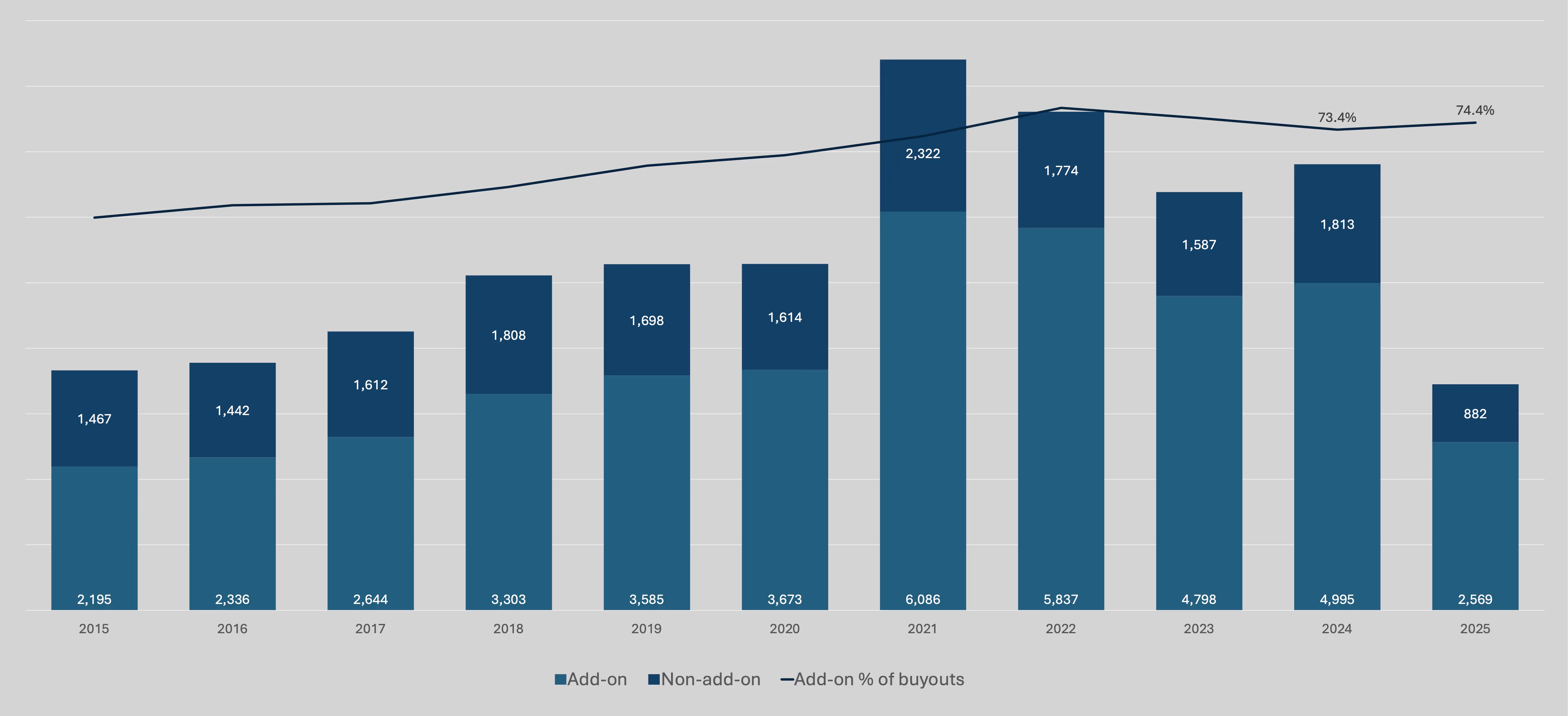

Add-on acquisitions continue to make up the lion’s share of US PE buyout activity. Through H1 2025, add-ons accounted for 74.4% of all buyouts, representing a slight increase from 2024’s 73.4% figure and close to the highest recorded amount of 76.7% in 2022. With a challenging exit environment and tempered valuation expectations, PE funds remain highly active in accretive, cost-effective add-ons to drive inorganic growth as organic growth stalls.

What This Means for NAV Lending

Given their nature, add-on acquisitions typically occur later in fund lifecycles than platform investments. Consequently, funds are more likely to have limited dry powder available to fund add-ons, and NAV facilities present an attractive means to fund the investments by leveraging their broader, mature portfolios.

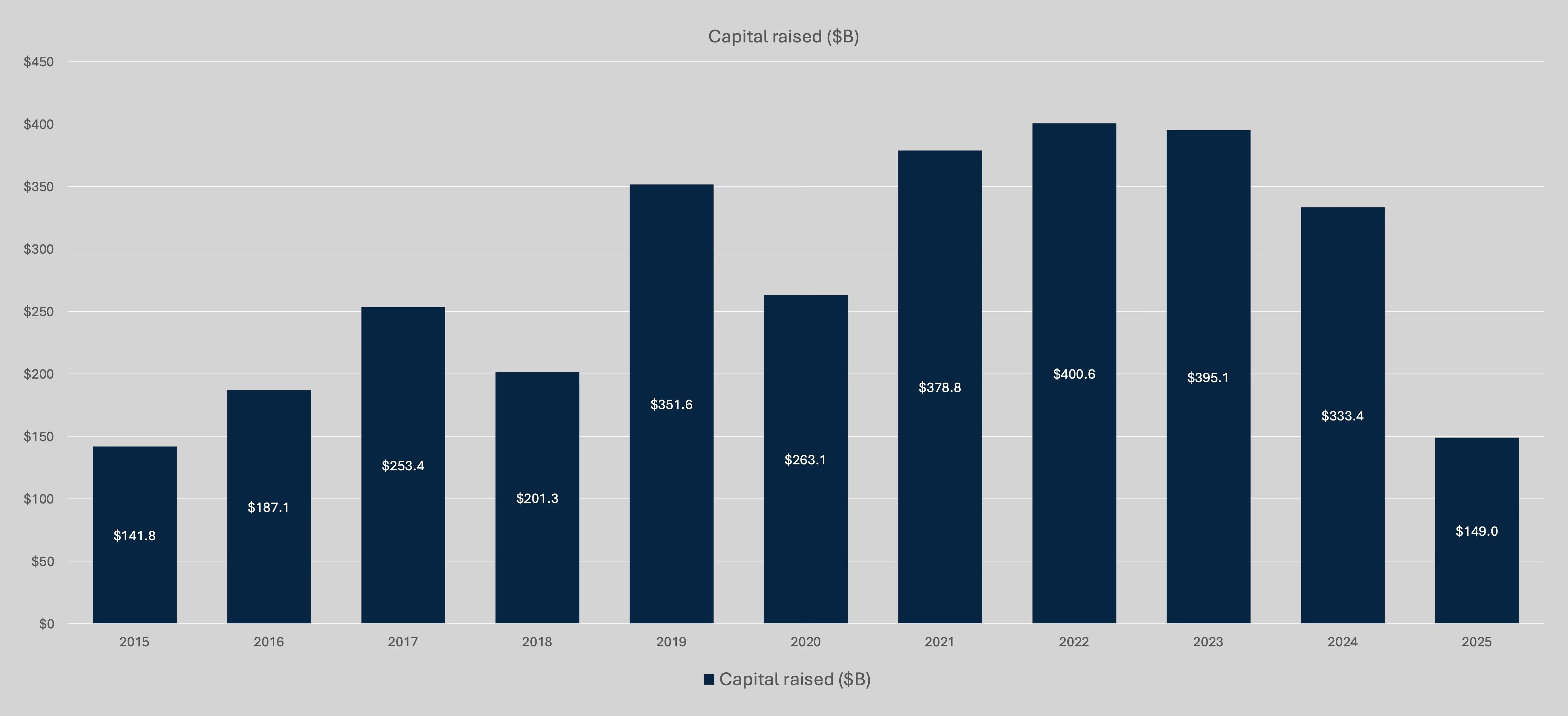

Q2 2025 saw an uptick in fundraising activity with ~$149bn raised for the year, relative to only ~$57bn through Q1. However, the H1 2025 total of ~$149bn is below the ~$155bn raised in H1 2024, and the current fundraising pace would place the year’s total ~$35bn below 2024’s ~$333bn raised. Additionally, 2025 fundraising has been driven by megafunds with ~59% of capital raised in 2025 going to funds over $5bn, relative to only ~40% in 2024. Continued economic uncertainty has depressed fundraising momentum with investors particularly cautious allocating capital to smaller funds.

What This Means for NAV Lending

With limited fundraising activity in 2025, sponsors will use NAV loans as a bridge to fundraising closes, enabling them to complete investments while continuing fundraising efforts.

Deal activity in Q2 2025 decreased from a strong Q1 with ~$105bn in total activity relative to ~$207bn in Q1. The YTD total of ~$311bn is already above 2022 and 2023 totals and on track to outpace 2024’s total of ~$376bn. Notably, H1 2025’s exit count of 470 remains below H1 2024’s total of 619, reflecting the continuation of the trend that sponsors are only bringing their highest quality assets to market. In line with this, median TTM EV / EBITDA valuation multiples remained at 12.8x EV / EBITDA compared to 13.0x in 2024.

What This Means for NAV Lending

The trend of private equity funds struggling to exit non-top performing portfolio companies will continue to drive demand for NAV loans as a means of injecting defensive or offensive capital to protect or grow asset values.

With continued market uncertainty, H2 2025 has the chance to produce a strong rebound in exit activity with resilient valuation, but there remains the risk of a more challenging period ahead due to:

- Continued uncertainty with tariffs and their potential impact on consumer spending and margins for import-exposed businesses could lead to continued slow exit activity, driving capital needs for portfolio companies that can be provided via NAV loans for mature funds with limited dry powder.

- Fundraising challenges have continued, particularly for middle market sponsors, driving demand for NAV loans to bridge capital needs for new funds.

- Valuations remain high, as seen in Q1 and 2024, reflecting sponsors exiting only their best assets and leaving a backlog of underperforming assets. These assets will need capital injections and add-ons, as seen in the large amount of add-on acquisitions, to expand valuations and drive profitable exits.

The NAV lending market remains robust in H2 2025 with sponsors pursuing accretive add-on and platform acquisitions while also stabilizing their portfolios and fundraising campaigns under a difficult and uncertain macroeconomic backdrop.

Recent Hark Capital Deals Closed

$65 million Fund Loan to PE Sponsor

- Hark funded $65 million to a US-based PE fund to refinance debt at two portfolio investments and provide additional balance sheet cash.

$20 million Fund Loan to Fund of Funds

- Hark funded $20 million to a US-based Fund of Funds to refinance the Fund’s subscription facility and fund capital calls from its underlying fund investments.

$50 million Fund Loan to PE Sponsor

- Hark funded $50 million to a US-based PE fund focused on the healthcare industry.Proceeds were used to fund a new platform investment for the fund as well as providing additional balance sheet cash to support additional follow-on investments.

$8 million Fund Loan to PE Sponsor

- Hark funded $8 million to a Canadian LMM PE fund and one portfolio company.Proceeds were used to support an add-on acquisition at one of the fund’s portfolio companies and provide additional liquidity to the fund.

$58 million Fund Loan to PE Sponsor

- Hark funded $58 million to a US-based PE fund focused on the business services and consumer industries. Proceeds were used to support an additional platform investment.